★★★ A Free Resource for Federal Employees Nationwide ★★★

How to Calculate Your FERS Pension

Download a free pdf FERS pension calculator for a clear picture of what you can expect to earn in retirement.

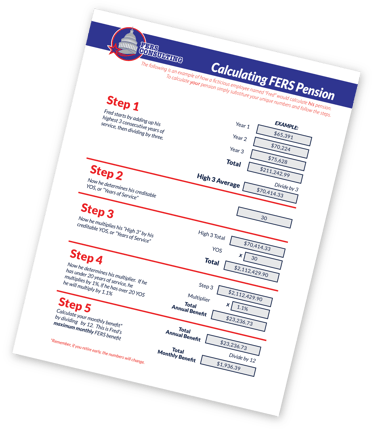

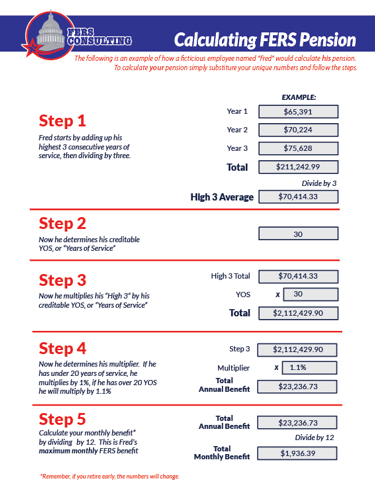

Your pension based on your length of service and the highest average basic pay you earned during any 3 consecutive years of service, also known as your “High-3” (or continuous 36 months). These three years are usually your final three years of service, but can be an earlier period, depending on your circumstances. To determine your length of service, add all your periods of creditable service, then eliminate any fractional part of a month from the total. Your creditable federal service, including:

Civilian service

Military service you paid deposit for

Sick leave (converted to additional service time)

Your basic pay includes increases to your salary for which retirement deductions are withheld, such as shift rates. It does not include payments for overtime, bonuses, etc.

Pension Calculation Fundamentals

A FORMULA BASED ON AVERAGE PAY & YEARS OF SERVICE

Standard FERS (Code K) Pension Options

Your pension is designed to make up 20-30% of your working salary. Your Social Security is also designed to replace around 20-30% of your working salary. Your TSP funds are designed to help fill the rest of your income needs in retirement. Every paycheck you contribute .8% towards your FERS Pension and 6.2% towards Social Security. At retirement you will select one of three retirement options:

OPTION 1 (Unreduced/Maximum): This option pays for LIFE OF THE EMPLOYEE ONLY. It is the largest pension amount an employee can possibly receive, however, once the employee dies, there is no payout to a beneficiary, regardless of the balance of their annuity.

UNDER 20 Years of Service - Highest 3 consecutive years of salary x Years Of Service x 1% = Your Annual Benefit

OVER 20 Years of Service - Highest 3 consecutive years of salary x Years Of Service x 1.1% = Your Annual Benefit

Click to Download a Free Pension Calculator

OPTION 2 (Maximum/Survivor):

This option allows the FERS Employee to select a beneficiary that would receive their FERS benefit if the employee were to die first. This option will REDUCE the employee's monthly pension by 10% as long as they are alive. The pension will be reduced again, should the employee outlive their beneficiary.

Example - During Employee's Lifetime assuming the original maximum benefit was $50,000:

Maximum benefit: $50,000/yr

Reduction factor: - 10% (or -$5,000)

Total payout: $45,000

The employee's pension is reduced because payments are being extended to continue, covering two lives.

What happens to the pension amount if the employee dies before their beneficiary? Under OPTION 2, if the FERS employee dies first, the pension payment is further reduced (-50% of your original maximum payout - See the following example).

Example - After the Employee Dies assuming the original maximum benefit was $50,000:

Maximum benefit: $50,000/yr

Reduction factor: - 50% (or -$25,000)

Total payout: $25,000

In this example, the pension that the beneficiary would receive until their death would be reduced to $25,000, paid out over the course of twelve months.

OPTION 3 (Partial/Survivor):

This option also allows the FERS employee to select a beneficiary that would receive their FERS benefit if the employee were to die first. This option will reduce the employee's maximum benefit by 5% as long as the employee is alive.

Example - During Employee's Lifetime assuming the original maximum benefit was $50,000:

Maximum benefit: $50,000/yr

Reduction factor: - 5% (or -$2,500)

Total payout: $47,500

The employee's pension is reduced because payments are being extended to continue, covering two lives.

What happens to the pension amount if the employee dies before their beneficiary? Under OPTION 3, if the FERS employee dies first, the pension payment is further reduced to 25% of the original maximum payout - see the following example).

Example - After the Employee Dies assuming the original maximum benefit was $50,000:

Maximum benefit: $50,000/yr

Reduction factor: - 75% (or -$37,500)

Total payout: $12,500

In this example, the pension that the beneficiary would receive until their death would be reduced to $12,500, paid out over the course of twelve months.

Click the example to enlarge

The computation of benefits can vary greatly depending on your personal circumstances and which of the three retirement options you choose. In this overview we have covered some basic computations for Code K, traditional FERS members. However if your circumstances are not listed on this page it is recommended that you schedule an appointment with a licensed federal retirement consultant below. You can also consult the official Office of Personnel Management guidelines HERE.

DIGGING DEEPER

Professional, Official Assistance

Planning the right moment to retire under the Federal Employees Retirement System (FERS) is one of the most important decisions a federal employee will make—and it’s not always simple. Between Minimum Retirement Age (MRA) rules, service-year requirements, early-out options, and special provisions, understanding when you’re truly eligible to retire can feel overwhelming. FERS Consulting helps federal employees cut through the confusion by providing clear, accurate, and personalized guidance, so you can confidently map out your retirement timeline and make informed decisions about your benefits and financial future.

Understand Your Permanent FERS Pension Options

CUT THROUGH CONFUSION

Contact Us

Have questions about your federal retirement? We’re here to help. Fill out the form below and a licensed FERS specialist will reach out with clear, personalized guidance tailored to your service, benefits, and retirement goals. Your path to confident retirement planning starts here.

CONSULTATIONS ARE FREE

Personalized guidance for federal retirement benefits.

© 2022-2026. All rights reserved. | Privacy

CONTACT

HEADQUARTERS

LEGAL

New Smyrna Beach, FL

FERS Consulting is not affiliated or endorsed by the Federal Government.