★★★ A Free Resource for Federal Employees Nationwide ★★★

What is the Role of the Thrift Savings Plan (TSP)?

Similar to a 401(k) in the private sector, your TSP plays a central role in the Federal Employees Retirement System

The Thrift Savings Plan (TSP) is a retirement savings and investment plan for federal employees and members of the uniformed services, including the Army, Navy, Air Force, Marine Corps, Coast Guard, and certain other federal agencies.

It is designed to help participants save and invest for their retirement years. The TSP is a key component of the retirement benefits offered to federal employees and service members. Federal employees have the opportunity to save part of their income for retirement, receive matching agency contributions and reduce their current taxes.

What is the Thrift Savings Plan?

SAVE PART OF YOUR INCOME FOR RETIREMENT

Thrift Savings Plan (TSP):

Voluntary Retirement Savings: The TSP allows eligible participants to voluntarily contribute a portion of their salary toward their retirement savings. Contributions are made on a pre-tax or Roth basis, providing participants with options for reducing their current taxable income or potentially receiving tax-free withdrawals in retirement.

Tax-Advantaged Savings: Contributions to the traditional TSP are tax-deferred, meaning you don't pay taxes on the contributions or any investment earnings until you withdraw the funds in retirement. Roth TSP contributions are made with after-tax dollars, and qualified withdrawals in retirement are tax-free.

TSP Investment Funds: The TSP offers a selection of low-cost investment funds, including both individual funds that cover different asset classes (such as stocks, bonds, and government securities) and Lifecycle Funds (L Funds) that automatically adjust the investment mix based on your expected retirement date. The different funds vary in levels of risk. The funds are listed here in order, from least to most risk: G, F, C, S & I

PRIMARY ROLES AND FEATURES

G-FUND: This fund is typically government securities, the least amount of risk making it nearly a cash account. Statistically, a little over 50% of all TSP accounts are in the G-Fund.

F-FUND: The F-Fund is an investment fund. It focuses on fixed-income securities, specifically bonds. F-Fund is designed to provide stability and income through bonds, making it generally less volatile than equity-based funds. However, it is subject to market risks, interest rate changes, and economic conditions that can impact it's performance.

C-FUND: The C-Fund is designed to provide participants with exposure to the U.S. stock market, specifically tracking the performance of the Standard & Poor's 500 (S&P 500) Index. The S&P 500 is a measuring tool. It helps us understand how well the 500 biggest and most important companies in the United States are doing.

About the TSP Funds

FEDERAL GROWTH FUNDS

The performance of the C Fund is directly tied to the performance of the S&P 500 Index. If the index goes up, the C Fund's value generally increases; if the index goes down, the C Fund's value generally decreases. The C-Fund is typically suited for participants with a long-term investment horizon, such as those who are early in their careers and have many years until retirement.

S-FUND: The S-Fund is designed to provide participants with exposure to small and mid-sized U.S. companies and track the performance of the Dow Jones Stock Market Index. The Dow Jones is like the S&P 500, only it tracks the performance of a small group of 30 big, well-known companies. These companies are leaders in their industries. It's an older index, however it is one of the most recognized indicators of the stock market's performance. As the index goes up or down, the value of the S-Fund generally follows suit. It is typically suited for participants with a long-term investment horizon, such as those who are early in their careers and have many years until retirement.

I-FUND: The I-Fund is designed to provide participants with exposure to international stocks and track the performance of the MSCI EAFE Index. The MSCI EAFE is a widely recognized tool that measures the performance of markets in developed countries located in Europe, Australasia & the Far East (EAFE). is generally suited for participants with a longer investment horizon who are willing to accept the potential for higher returns along with greater risk.

L-FUND (Lifecycle): L-Funds are designed for participants who prefer a more automated approach to investing. Participants simply choose the L-Fund that corresponds to their expected retirement date, and the fund automatically adjusts its allocation over time. Allocation means deciding how much of your investment money you'll put into the different TSP fund types. (For example you may want 50% in the G, 20% in F, 10% in each C, S & I). The idea is to create a balanced plan that suits your goals and needs. If you choose a Lifecycle Fund (L-Fund) The percentage of your investments will start off with more market exposure, then get less and less risky as you approach your retirement date. This happens automatically, you do not have to choose individual stocks or bonds.

L-FUND (Income): The L Income Fund is designed for participants who are already retired or very close to retirement and are looking for a conservative and stable investment option that provides income in retirement.

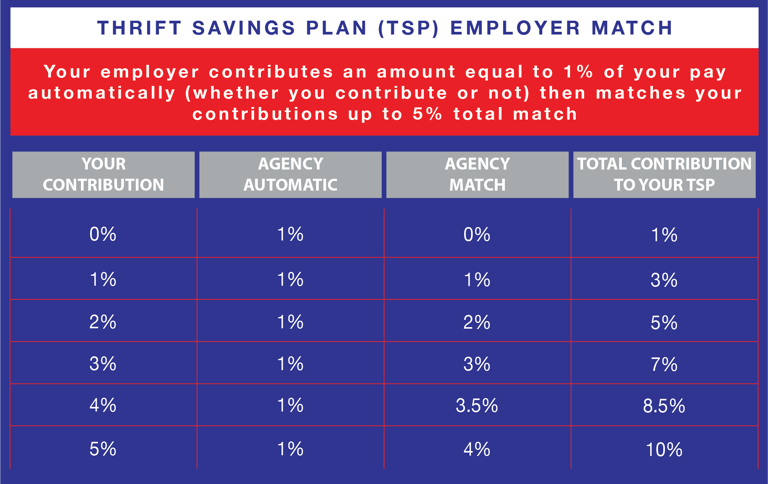

Some federal agencies and military branches offer employer matching contributions for their employees' TSP contributions. The matching policy varies by agency and service branch. Generally there is a true match up to 5% of your contribution - free money! (Not applicable for CSRS employees) The great news is that you will get TSP Statement whether you contribute or not - because your employer puts in 1% of your salary no matter what! Whether the 1% contribution from your employer is enough to fund your retirement will depend on your personal circumstances. However, the matching element of the TSP is a huge advantage for participants and an excellent way to create a 3rd source of retirement income. This chart should help make sense of how the match works.

TSP: Matching Funds

EMPLOYER MATCHING (FOR SOME PARTICIPANTS)

Click to enlarge

Portability: If you leave federal service, you can keep your TSP account active and continue to manage and contribute to it. You can also roll over your TSP balance into an eligible IRA or another employer's retirement plan.

Low Costs: The TSP is known for its extremely low administrative costs and investment fees, making it an attractive option for retirement savings.

Access to Funds: While the primary purpose of the TSP is retirement savings, there are certain circumstances (such as financial hardship, age 59½ or meet the minimum retirement age and minimum years of service requirements) that allow for penalty-free withdrawals, although since the funds are tax-qualified (Meaning you didn't pay taxes on the income yet) you will be required to pay taxes once funds are withdrawn. The exception would be if your TSP funds were allocated in a Roth account or you are rolling the funds into a different tax-qualified account like an IRA, 403(b), 457(b) etc.

An Excellent Way to Save for Retirement

MORE TSP FEATURES

Consistency and Long-Term Focus: The TSP encourages a disciplined approach to retirement savings by automating contributions from your paycheck. Its investment options are designed to support long-term growth and retirement planning.

Education and Resources: The TSP provides educational materials, resources, and tools to help participants understand their investment options, make informed decisions, and plan for retirement. However, federal employees can gain the most benefit from meeting with a licensed federal Retirement consultant. A credited financial professional can provide a full benefit analysis that shows your FERS, SS, TSP and other investments combined in one report. They can then recommend a plan based on your personal goals and circumstances. This is nearly always a free service. The publishers of this website can provide more information if desired.

Contact Us

Have questions about your federal retirement? We’re here to help. Fill out the form below and a licensed FERS specialist will reach out with clear, personalized guidance tailored to your service, benefits, and retirement goals. Your path to confident retirement planning starts here.

CONSULTATIONS ARE FREE

Personalized guidance for federal retirement benefits.

© 2022-2026. All rights reserved. | Privacy

CONTACT

HEADQUARTERS

LEGAL

New Smyrna Beach, FL

FERS Consulting is not affiliated or endorsed by the Federal Government.